If you’re already on a floating-rate home loan in India, you’ve probably felt the pinch of rate resets. The fastest way to reduce the total interest you’ll pay—and own your home sooner—is to treat refinancing as a disciplined, numbers-first project. Below are five proven strategies built for existing floating-rate borrowers, with practical math, checklists, and negotiation scripts you can copy to reduce home loan interest in India without guesswork.

A quick regulatory snapshot (India)

- Multiple reputable sources report that, from January 1, 2026, the RBI has banned prepayment/foreclosure charges on floating-rate loans to individual borrowers (including home loans). See the summaries by Business Today in RBI removes prepayment charges on floating-rate loans (2025) and the explainer on Insights on India (2025). Note: An SME/legal reviewer should insert the exact RBI circular link and clause before publication.

- Lenders still charge processing fees, legal/valuation, CERSAI, and state stamp/franking/MOD when you switch to a new lender. These vary by bank and state; always verify on the official schedule.

- Fixed-rate loans may have prepayment charges per contract. This post focuses on floating-rate borrowers.

Strategy 1: Negotiate a rate cut with your current lender (repricing)

Start here. Repricing avoids the paperwork of a balance transfer and can deliver most of the benefit if your lender matches market rates. Request a “rate match” to the lender’s current new-customer rate for your risk bucket, ask for the conversion fee to be waived or capped, and request your spread over the benchmark (repo/MCLR/RLLR) be reset to parity with new originations. Anchor your request with two current quotes you’ve collected from other banks.

Copyable email

Subject: Home loan rate repricing request (Account XXXX)

Hello [Relationship Manager/Branch],

I’m on a floating-rate home loan linked to [benchmark] at [current rate]%. Based on market quotes from [Bank A] and [Bank B] at ~[lower rate]% for my profile, I request a repricing to [target rate]% and a waiver/cap of the conversion fee. Kindly confirm the new spread over [benchmark] and the applicable fee in writing.

Thank you, [Name]

Quick phone script

- “I’m seeing market quotes at around [rate]%. Can you match that today? If there’s a conversion fee, please confirm the exact amount and the new spread in writing.”

Reference example: Axis Bank’s fee schedule lists repricing fees (e.g., 0.5% of outstanding, minimum ₹10,000) for certain switches; see the official Axis Bank home loan fees and charges PDF.

Strategy 2: Consider a balance transfer (refinance) to a lower-rate lender

When repricing stalls or the rate gap is large, compare an external switch. Treat it like a small project with clear steps and costs.

Step-by-step checklist

- Collect quotes and fee sheets from 2–3 lenders (rate, processing fee, legal/valuation, stamp/franking/MOD, CERSAI, GST).

- Request a provisional/instant sanction from your preferred lender, subject to verification.

- Ask your current lender for a foreclosure/closure letter and a list of documents they hold.

- Submit KYC, income proofs, last 6 months’ bank statements (with EMI debits), property title/sale deed copies, and your loan statement/outstanding certificate.

- Complete legal and valuation checks; clarify any state levies (stamp/franking/MOD).

- Coordinate disbursement and document handover; confirm the first EMI date and the amortization schedule.

- After closure, verify that your old loan is reported as closed by the bureaus.

Typical fees (illustrative ranges—confirm before you sign)

| Lender | Processing Fee (typical) | Notes |

|---|---|---|

| SBI | NIL (per aggregator snapshot) | Cross-check SBI’s official schedule; see Paisabazaar SBI BT page. |

| ICICI Bank | 0.50%–2.00% of amount or ₹3,000 (higher) + taxes | See ICICI home loan service charges. |

| Axis Bank | Up to 1% or ₹10,000 (higher) + GST | See Axis processing fee explainer. |

| HDFC Bank | Up to 1.50% or ₹4,500 (min retention) | Aggregator summary; verify on HDFC’s official site: HDFC BT snapshot. |

Tip: Avoid bundled add-on insurance unless you need it; confirm opt-out in the sanction letter.

Strategy 3: Do the break-even math to reduce home loan interest in India

Here’s the simple rule: Don’t switch unless the savings comfortably beat the total switching costs within a reasonable time.

Key formulas

- EMI ≈ P × r × (1 + r)^n / [(1 + r)^n − 1], where P = outstanding principal, r = monthly rate, n = remaining months.

- Monthly saving ≈ EMI at current rate − EMI at new rate (same remaining tenure for a clean comparison).

- Months to break even = Total switch costs / Monthly saving.

Plug-and-play template (copy to a spreadsheet)

| Item | Value |

|---|---|

| Outstanding principal (P) | 3,500,000 |

| Remaining tenure (months) | 144 |

| Current annual rate (%) | 9.25 |

| New annual rate (%) | 8.50 |

| Total switching cost (₹) | 25,000 |

| EMI at 9.25% | =PMT(9.25%/12,144,3500000) |

| EMI at 8.50% | =PMT(8.50%/12,144,3500000) |

| Monthly saving | =EMI_9.25 − EMI_8.50 |

| Months to break even | =Total Cost / Monthly Saving |

Worked examples (illustrative, Jan 2026 assumptions)

- Small balance: ₹15 lakh outstanding, 72 months left, 9.20% → 8.60%; fees ₹12,000. Approximate EMI drops by ~₹500–₹700; break-even often within 15–24 months. If your tenure left is under ~5 years and the rate gap is ≤ 0.25%, consider repricing instead of switching.

- Medium balance: ₹35 lakh, 144 months left, 9.25% → 8.50%; fees ₹25,000. EMI can drop by ~₹1,400–₹1,700; break-even often in 6–12 months, with six-figure total interest saved over the remaining life.

- Large balance: ₹80 lakh, 216 months left, 9.50% → 8.60%; fees ₹45,000. EMI may drop by ~₹4,500–₹5,500; break-even typically under 6–9 months, with very large lifetime savings.

Strategy 4: Optimize structure if you stay put

If a full transfer doesn’t pencil out, you can still reduce home loan interest India with structure tweaks. If cash flow allows, keep the EMI the same after a rate cut (don’t reduce it); you’ll shorten the effective tenure and trim total interest. Some lenders offer OD/offset accounts; parking surplus here reduces interest on the daily balance while keeping liquidity. With floating-rate loans to individuals, prepayment penalties are reportedly banned from Jan 2026 per secondary sources cited earlier—so channel windfalls toward principal to curb interest accrual.

Considering alternatives: If your goal is liquidity for business or life events, a Loan Against Property (LAP) may be an alternative to repeated refinancing. For a neutral primer on prudent use of LAP, see the LAP & Smart Leverage Advisory overview.

Strategy 5: Guardrails—when not to refinance

- Short remaining tenure: If you’ve got fewer than ~36 months left, the break-even may stretch beyond your useful horizon.

- Tiny rate delta: If the gap is under ~0.25–0.35%, a repricing with your current lender is usually more sensible.

- High state levies or ancillary costs: In some states, MOD/stamp/franking can swing the math; verify first.

- Imminent rate cycle shifts: If repo cuts are widely expected and your current loan is responsive to the benchmark, waiting or repricing may capture much of the benefit.

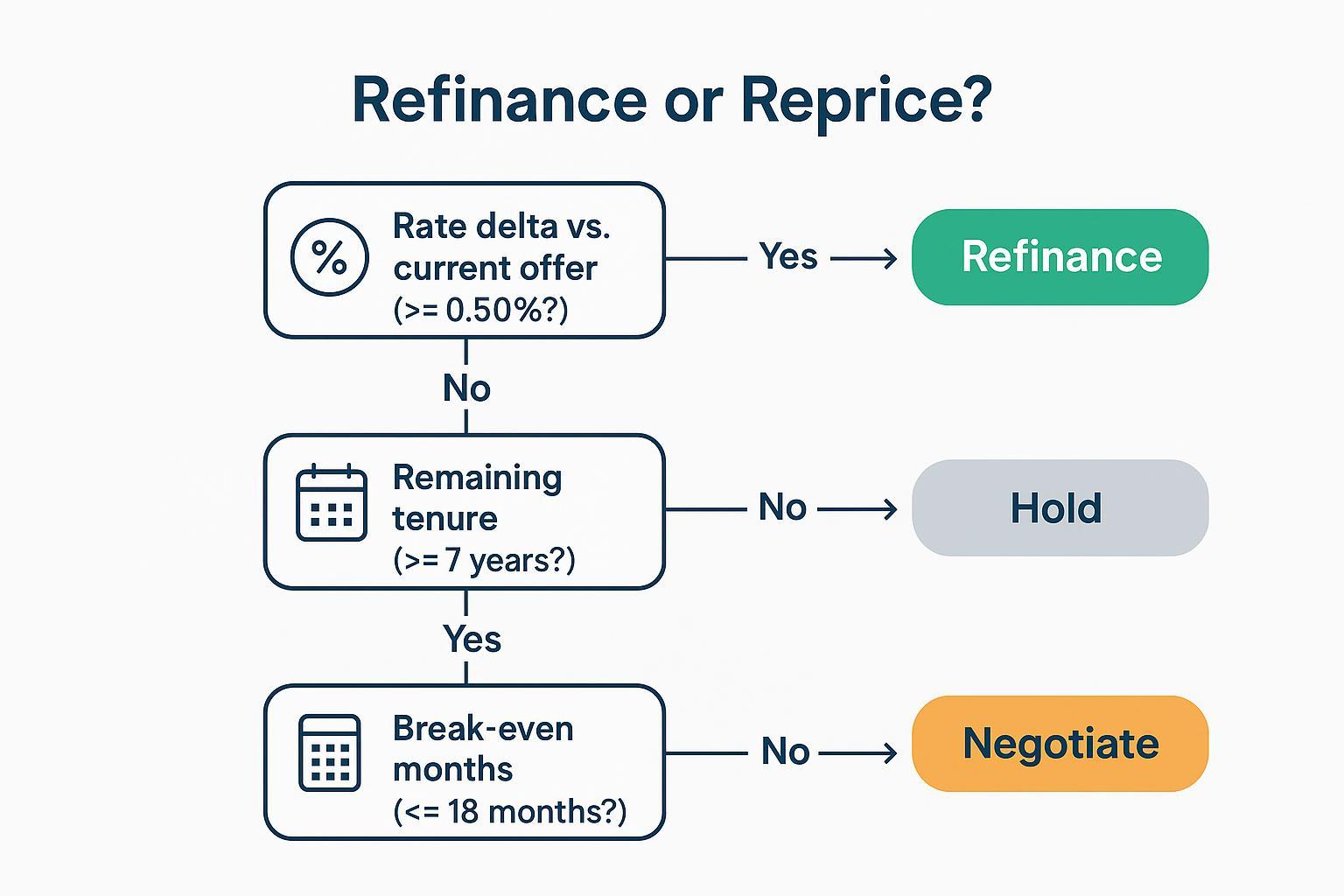

Decision rules of thumb

- Refinance: Rate gap ≥ 0.50%, remaining tenure ≥ 7 years, and break-even ≤ 18 months.

- Negotiate (repricing): Rate gap ~0.25–0.50% or tenure 3–7 years.

- Hold: Rate gap < 0.25% or tenure < 3 years, unless switching fees are near zero.

Practical example: Neutral tool-supported analysis

Disclosure: SSfinadvisory is our product.

When we run a balance-transfer analysis, we model your current amortization vs. the target rate with identical remaining tenure, overlay lender quotes for processing/legal/valuation and state levies, and compute months-to-break-even plus lifetime interest saved. If you want to see what that workflow looks like in practice, the methodology aligns with what’s described on the Home Loan Strategy & Optimisation page. Use it as a reference while building your own spreadsheet.

FAQ

- Will a balance transfer hurt my credit score? A new inquiry and account can dip your score a few points temporarily. With on-time EMIs, scores typically recover. See CRIF High Mark’s explainer on consolidation and credit reports and Equifax India’s help center.

- How long does a transfer take? Straightforward cases close in ~15–30 days once documents are in order, based on lenders’ own timelines—see ICICI’s average home loan processing time overview and Axis’s transfer procedure explainer.

- Do I pay prepayment penalties to close my old floating-rate home loan in 2026? Secondary sources indicate “no” for individual floating-rate loans from Jan 1, 2026, but please verify against the RBI’s primary circular once published/linked.

- What fees will I pay at the new lender? Processing fee, legal/valuation, CERSAI, and state stamp/franking/MOD plus GST. Confirm on the lender’s latest fee schedule; see examples under Strategy 2.

- Can the new lender force bundled insurance? Some lenders bundle add-ons; request opt-out for anything you don’t need. Ensure the sanction letter reflects your choice.

- Is switching worth it if I plan to sell in 2–3 years? Usually not—your break-even may come too late. Try repricing instead.

Author and review notes

This article was prepared by a retail-lending advisor with 20+ years of banking experience. Calculations are illustrative and based on assumptions dated January 2026. An SME/legal reviewer should insert the link to the RBI circular on the prepayment-charge rule and validate fee examples against the current official schedules before publication.

Sources and references

- RBI policy (secondary confirmations): Business Today coverage (2025); Insights on India explainer (2025).

- Lender rates/fees and workflows: SBI interest rates page; ICICI home loan service charges; Axis processing fee explainer; Axis fees PDF; ICICI processing time; Axis transfer procedure. External aggregator snapshots are used sparingly and flagged above for verification before action.