The most common regret I hear: “I wish I had started prepaying in year 1, not year 8.”

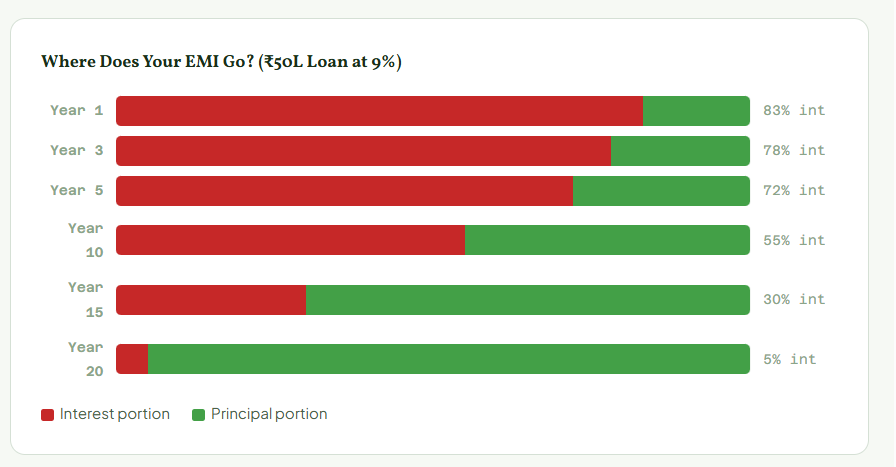

That sentence — or some version of it — comes up in almost every initial consultation. By the time most borrowers think about prepayment, they have already spent the most expensive years of their loan paying maximum interest and minimum principal. The chart above tells the whole story: in Year 1, 83 paise of every rupee you pay in EMI goes to the bank as interest. Only 17 paise reduces your actual debt.

This post explains exactly why prepaying in the first five years delivers 2–3× the savings of prepaying later — with the hard numbers to prove it. If you are in the early years of your loan, this is the most important post in our entire prepayment series.

How Amortisation Works Against You in Early Years

Every home loan in India uses a reducing-balance amortisation schedule. Your EMI stays constant, but the split between interest and principal shifts over time. In the early years, the outstanding balance is at its highest, so interest charges are at their peak — and most of your EMI services that interest rather than reducing the principal.

On a ₹50 lakh loan at 9% for 20 years, your EMI is ₹44,986. In Month 1, the split is approximately ₹37,500 interest and ₹7,486 principal. That means only 16.6% of your first payment actually reduces what you owe. The rest — ₹37,500 — goes straight to the bank.

By Month 120 (Year 10), the split shifts to roughly ₹24,750 interest and ₹20,236 principal. By Month 200 (Year 17), it flips entirely — ₹9,500 interest and ₹35,486 principal. The loan becomes progressively cheaper to carry, but by then you have already paid the bulk of the total interest.

The implication for prepayment: When you prepay in Year 1, you are removing principal that was generating ₹37,500/month in interest charges. When you prepay the same amount in Year 10, you are removing principal generating only ₹24,750/month. Same rupees paid, vastly different impact. This is why timing is everything.

Year 1 vs Year 10 Prepayment — The Shocking Difference in Savings

Let me show you the multiplier effect — how many rupees of interest each rupee prepaid saves, depending on when you prepay.

Year 1

2.8×

₹1 prepaid → ₹2.80 saved

Year 5

1.9×

₹1 prepaid → ₹1.90 saved

Year 10

1.1×

₹1 prepaid → ₹1.10 saved

Year 15

0.3×

₹1 prepaid → ₹0.30 saved

The multiplier drops from 2.8× in Year 1 to just 0.3× in Year 15. That is nearly a 10× difference in impact. A ₹1 lakh prepayment in Year 1 saves ₹2.8 lakhs. The same ₹1 lakh in Year 15 saves just ₹30,000. This is not a marginal difference — it is the difference between a strategy that transforms your loan and one that barely moves the needle.

The Interest-to-Principal Ratio Explained Simply

Think of your EMI as a pie sliced between the bank (interest) and your equity (principal). In Year 1, the bank gets 83% of the pie. By Year 10, the split is roughly 55:45. By Year 15, you finally get the larger slice at 70%.

Prepayment does not change the pie — it changes the base on which future pies are calculated. Reduce the principal by ₹2 lakhs in Year 1, and every future month’s pie is calculated on a base that is ₹2 lakhs smaller. Over 228 remaining months, the cumulative impact is enormous. Reduce the same ₹2 lakhs in Year 15, and only 60 months of reduced-base benefit remain — plus the monthly interest charge was already much lower.

This is the engine behind the 13th EMI strategy and the annual bonus deployment being most effective when started from Year 1.

Real Numbers: ₹50L Loan — ₹2L Prepayment at Year 1 vs Year 10

₹2 Lakh Prepaid in Year 1

Loan₹50L at 9%, 20 years

Prepayment₹2,00,000 (Year 1)

Interest Saved (over remaining tenure)₹5,22,000

Tenure Reduced~12 months

Multiplier2.6× (₹2L in → ₹5.2L saved)

₹2 Lakh Prepaid in Year 10

Loan₹50L at 9%, 20 years

Prepayment₹2,00,000 (Year 10)

Interest Saved (over remaining tenure)₹1,82,000

Tenure Reduced~5 months

Multiplier0.9× (₹2L in → ₹1.8L saved)

The gap: ₹3.4 lakhs. Same ₹2 lakh payment, same loan, same rate — but a ₹3.4 lakh difference in outcome purely because of timing. Over multiple prepayments across the early years, this gap compounds to ₹6–12 lakhs depending on the total amount prepaid and how early you begin.

Run your own numbers using our free prepayment calculator — it lets you set the prepayment start year so you can see the exact impact at any stage of your loan.

What If You Could Not Prepay Early? Recovery Strategies

If you are already in Year 7, 8, or even 10 — do not despair. The window is narrower, but meaningful savings are still achievable. Here is the recovery playbook:

The wrong response: “It is too late, so there is no point.” This is the most expensive misconception in home loan management. Even in Year 10, a ₹2L prepayment saves ₹1.8L — that is still a guaranteed 90% return. It is lower than Year 1, but it is better than any fixed deposit or savings account.

Compensate with larger amounts. If you missed the early years, increase your annual prepayment to close the gap. Where a Year 1 borrower might prepay ₹50K/year, a Year 8 borrower should aim for ₹1–1.5L/year to achieve comparable total savings.

Combine with a balance transfer. If your rate is not competitive, a balance transfer plus prepayment combination can recover significant ground. Lowering your rate by 1% in Year 8 and then prepaying aggressively can still save ₹6–10 lakhs.

Use the step-up approach. Start with whatever you can and increase each year. The step-up EMI strategy works at any stage — it is just most powerful when started early.

Are You in the First 5 Years? Act Now.

This is your highest-leverage window. I will build you a custom prepayment plan that captures the maximum multiplier effect while your loan is still young.Get Your Custom Prepayment Plan

How to Maximise First-5-Year Prepayments on a Tight Budget

The irony of the early-years window is that it coincides with the phase when most borrowers have the tightest budgets — you have just bought a home, possibly furnished it, and your salary is still growing. Here are practical ways to fund prepayments without financial strain:

- Start with the 13th EMI method. Set aside just 1/12th of your EMI each month (roughly ₹3,000–₹4,000 for a ₹40–50L loan) in a separate account. Prepay the accumulated amount annually. It is the lowest-barrier entry point. Full strategy in our extra EMI post.

- Route 50% of every raise to prepayment. When your salary increases by ₹5,000/month, redirect ₹2,500 to prepayment savings. You never miss money you have not started spending. This is the voluntary step-up approach.

- Deploy 40–60% of your annual bonus immediately. Make the prepayment within the first week of receiving the bonus — before the money finds other uses. See our bonus deployment guide for the optimal split.

- Liquidate low-yield savings. If you have ₹1–2 lakhs sitting in a savings account earning 3–4%, prepaying your 9% loan is an immediate 5–6% guaranteed improvement. Keep 6 months of expenses as an emergency fund and deploy the rest.

- Skip one major discretionary expense per year. One international holiday deferred, one phone upgrade skipped, one car service delayed — the ₹30,000–₹80,000 saved, deployed as a Year 2 or Year 3 prepayment, generates ₹60,000–₹1.6 lakhs in interest savings over the loan’s life. The maths makes the trade-off obvious.

Frequently Asked Questions

Is it true that prepaying early on a home loan saves more?

Yes — significantly. In the first 5 years, 65–75% of your EMI is interest. Prepaying reduces the high-interest principal, and savings compound across 15+ remaining years. On a ₹50L loan at 9%, ₹2L prepaid in Year 1 saves ~₹5.2L; the same amount in Year 10 saves only ~₹1.8L. The multiplier drops from 2.6× to 0.9×.

How much can I save by prepaying ₹1 lakh in the first year?

On a ₹50L loan at 9%/20 years, a ₹1L prepayment in Year 1 saves approximately ₹2.6–2.8L in total interest and shortens tenure by 5–6 months. The multiplier effect is roughly 2.7× — every rupee prepaid saves nearly ₹3 in future interest.

What if I missed the early prepayment window?

Start now regardless. Prepayment in Year 7–10 still delivers a positive return. Compensate by increasing your annual amount, combining with a balance transfer if your rate is high, and using the step-up strategy. The best time was Year 1; the second best is today.

Can I still save significantly if I prepay in year 7 or 8?

Yes. A ₹2L prepayment in Year 7 saves approximately ₹2.5–3L. It is less than Year 1 but still a strong guaranteed return. Regular annual prepayments of ₹1–2L starting in Year 7 can still save ₹5–8L total and cut 3–4 years off your loan.

Does the early prepayment advantage apply to fixed-rate loans?

Yes — the amortisation maths is identical. Early years carry higher interest regardless of rate type. However, fixed-rate loans may have 2–3% prepayment charges, reducing the net benefit. For floating-rate loans (95%+ of Indian home loans), prepayment is penalty-free under RBI rules.

Your First 5 Years Are Ticking. Make Them Count.

I will build a custom prepayment schedule that captures the maximum multiplier effect for your specific loan, income, and budget. Book Free Consultation

About the Author: Somnath Sarkar is a home loan strategy consultant with 20+ years at Axis Bank and Deutsche Bank, specialising in prepayment planning, balance transfers, and interest optimisation.

Disclaimer: This article is for educational purposes only and does not constitute financial advice. Calculations are illustrative, based on standard reducing-balance amortisation at 9% p.a. Actual savings depend on your specific loan terms. Consult a certified financial planner before making decisions.

Last Updated: 20 May 2026 | First Published: 20 May 2026

© 2026 Somnath Sarkar. All rights reserved.