The legal due diligence stage (Step 4) is where most delays happen. Borrowers assume their documents are in order; the bank’s lawyer finds a 20-year-old intermediate deed that was never registered. I will show you exactly how to pre-empt every common issue before it derails your timeline.

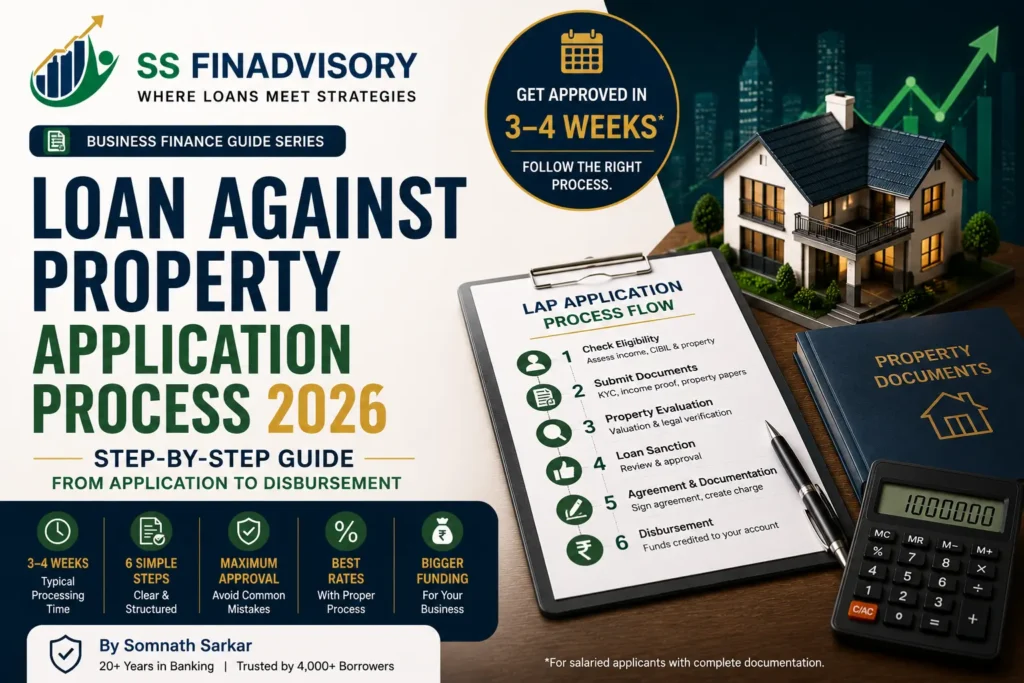

A LAP application feels opaque when you are going through it for the first time — you submit documents, then wait, then receive more questions, then wait again. This post demystifies all six stages, explains exactly what the bank is doing at each step, flags the negotiation leverage points you should use, and gives you a realistic timeline to plan against. By the end, you will know what to expect on any given day of your application, and how to move it forward.

STEP1

Pre-Application: Property Valuation & Eligibility Check

⏱ 3–5 daysNo CIBIL hitZero cost (usually)

Before submitting a formal application, confirm two things: your property qualifies for LAP, and your profile meets eligibility. This step is completely informal — no CIBIL inquiry, no commitment.

- Get an indicative property valuation from 1–2 channel partners or real estate consultants

- Pull your CIBIL report from cibil.com (free) and verify score is 700+

- Review property ownership — confirm registered sale deed is in your name

- Check for any existing mortgage on the property (deal-breaker for LAP)

- Calculate indicative eligible amount using the formula in our LAP Eligibility guide

Why this step matters: Spending 3 days upfront to confirm eligibility saves 3 weeks of a stuck application downstream. If you find issues (title gaps, CIBIL errors, existing mortgage), you can resolve them before applying — preserving your CIBIL score and avoiding processing fees on an application that would have failed.

STEP2

Lender Selection and Rate Negotiation

⏱ 5–7 daysSoft inquiries onlyCritical leverage stage

Get in-principle sanctions (soft inquiry based) from 3–4 lenders to compare rates and terms. Major banks (SBI, HDFC, Axis, ICICI) will issue indicative letters in 5–7 days based on your income and CIBIL. This is your leverage collection phase.

- Approach 3–4 lenders: mix of PSU bank (SBI), private bank (HDFC or Axis), and HFC (LIC Housing) for diverse options

- Request in-principle sanction (soft inquiry) — not a full application

- Compare rate, processing fee, LTV offered, and loan amount approved

- Use strongest offer to negotiate with your preferred lender

- Pick final lender based on net cost over 3 years, not just headline rate

Leverage Point

This is where most of your negotiation happens. Once you proceed to a full application at one bank, your leverage drops significantly — they know you are committed. Use the in-principle stage to extract the best possible terms before full submission. See our LAP rate negotiation guide for the exact script.

STEP3

Document Submission and Verification

⏱ 5–10 daysHard inquiry triggeredProcessing fee payable

Submit the full application with all documents. This triggers the formal process — a hard CIBIL inquiry, payment of the processing fee (or part of it), and allocation of a case number in the bank’s system. The bank’s credit team reviews KYC, income, and property documents for completeness and consistency.

- Submit complete KYC + income + property document set (see our LAP documents checklist)

- Pay processing fee (usually 50% upfront, 50% at sanction) or full amount as per bank policy

- Respond to any initial queries within 48 hours to avoid re-submission delays

- Bank’s credit team conducts income verification — phone/letter to employer or CA

- CIBIL report pulled and detailed review conducted

Critical in this phase: Any missing document restarts verification from scratch. It is much faster to take an extra 2–3 days upfront to ensure completeness than to submit a partial file and spend 2 weeks ping-ponging over missing items. Pre-verify your file with a checklist before submission.

STEP4

Legal and Technical Due Diligence

⏱ 7–14 daysMost common delay pointHandled by bank’s legal team

The bank’s empanelled lawyer conducts independent verification of your property’s legal status, and the panel valuer conducts an on-site property valuation. These two parallel tracks determine final sanction.

Legal due diligence includes:

- Title search across 30 years of ownership history from the sub-registrar office

- Encumbrance certificate verification confirming no prior mortgage or lien

- Municipal records search for property tax arrears, notices, or disputes

- Building plan and occupancy certificate verification

- Society/builder NOC authentication

- Issuance of legal opinion: Clear, With Observations, or Adverse

Technical due diligence (property valuation) includes:

- On-site inspection by panel valuer (1–2 days from instruction)

- Verification of construction quality, age, and condition

- Comparison with recent sale transactions in the locality

- Final market value assessment (may differ from your expectation by ±10%)

Pre-empt common issues: Before this stage even begins, get your lawyer to do a 2-hour review of your title chain and identify any gaps. If there is a missing intermediate deed or an unregistered historical transfer, address it now via a registered rectification deed or court declaration. Fixing it upfront saves 4–6 weeks versus addressing it under bank pressure later.

Want Someone to Guide You Through Every Step?

I personally manage each stage — eligibility check, lender negotiation, document submission, legal liaison, sanction review, and disbursement follow-up. Most clients close in 20–25 days, not 45. Book a Free Application Review

STEP5

Loan Sanction and Agreement Signing

⏱ 3–5 daysFinal rate lockedNegotiation window closing

Once legal and technical DD clear, the credit committee issues the final sanction letter. This document specifies the final loan amount, interest rate, tenure, EMI, processing fee, and all terms. Review carefully before signing.

- Read the entire sanction letter — do not skim over annexures

- Verify loan amount, rate, tenure, EMI match what was agreed

- Check for any unexpected charges (insurance bundling, maintenance fees)

- Confirm prepayment terms — zero charges on floating rate per RBI rules

- Sign the loan agreement and executed hypothecation deed

- Submit original property documents to the bank (they will retain until closure)

Last Negotiation Chance

If the sanction letter has unexpected charges or terms slightly different from agreed, raise it now — the bank still has flexibility before documents are registered. Once MODT (next step) is filed, modifications become expensive. Commonly negotiated at sanction stage: insurance bundling (can usually be declined), specific fee line items, and rate conversion provisions.

STEP6

MODT Registration and Disbursement

⏱ 3–7 daysMoney hits your accountState-specific stamp duty

The final stage before disbursement. MODT (Memorandum of Deposit of Title) creates the bank’s legal charge on your property. It must be registered at the sub-registrar office with the applicable stamp duty. After MODT, CERSAI charge is created online, post-disbursement conditions are verified, and the loan amount is credited.

- Pay stamp duty on MODT (state-specific — 0.1% to 0.5% of loan amount)

- MODT document drafted by bank’s lawyer and executed

- Physical registration at sub-registrar office (borrower present)

- CERSAI registration completed online (₹500–₹1,500)

- Bank verifies all post-sanction conditions met

- Disbursement to your bank account or directly to supplier/existing lender

The money is credited within 2–3 working days after MODT registration. For most borrowers using LAP for general business or personal purposes, it is a straight credit to your bank account. For refinancing (paying off existing debt), the bank routes the payoff directly to your existing lender and disburses only the balance to you.

Timeline: What to Expect at Each Stage

| Stage | Salaried | Self-Employed | What Bank Is Doing |

|---|---|---|---|

| Step 1 — Pre-Application | 3–5 days | 3–5 days | No bank involvement |

| Step 2 — Lender Selection | 5–7 days | 5–7 days | Issuing in-principle letters (soft inquiry) |

| Step 3 — Application & Documents | 5–7 days | 7–12 days | Credit team reviewing all documents |

| Step 4 — Legal & Technical DD | 7–10 days | 10–15 days | Lawyer + valuer conducting independent checks |

| Step 5 — Sanction & Agreement | 3–5 days | 3–5 days | Credit committee decision and documentation |

| Step 6 — MODT & Disbursement | 3–7 days | 3–7 days | Stamp duty, registration, disbursement |

| TOTAL | 21–28 days | 28–42 days |

* Assumes clean documentation and no title issues. Missing documents or title chain gaps can add 2–4 weeks. PSU banks typically add 7–10 days versus private banks.

Frequently Asked Questions

How long does the LAP application take to process?

3–6 weeks end-to-end. Salaried with clean documentation: 21–28 days. Self-employed: 28–42 days (extra income verification). NBFCs like Bajaj Finance fastest at 15–25 days; PSU banks like SBI slowest at 35–50 days. Missing documents add 2–4 weeks at legal DD stage.

What is the legal due diligence process for LAP?

Bank’s empanelled lawyer conducts: (1) 30-year title search, (2) encumbrance certificate verification, (3) municipal records check, (4) society/builder record review, (5) statutory approval confirmation. Issues a “search and title” report — clear, with observations, or adverse. Takes 5–15 days; most common delay source.

Can I apply to multiple banks simultaneously for LAP?

Technically yes, but unwise. Each full application = hard CIBIL hit (10–15 point ding) and non-refundable processing fee. 3 parallel applications cost ~40 CIBIL points and ₹40K+ in fees. Better approach: get in-principle (soft inquiry) sanctions from 3–4 lenders, then proceed with full application at your top choice only.

Is pre-approval for LAP possible?

Yes. Major banks offer in-principle approval in 3–7 days based on income and CIBIL, without property verification. Valid 60–90 days. Confirms max eligible amount and indicative rate. HDFC, Axis, ICICI, Kotak have streamlined pre-approval processes. Useful for property negotiation leverage and qualification confirmation.

When is the loan amount actually disbursed?

After: (1) signed sanction letter, (2) executed loan agreement, (3) original property documents submitted, (4) MODT registered at sub-registrar, (5) CERSAI charge created, (6) post-disbursement conditions met. Then disbursement within 2–3 working days. For refinancing LAPs, bank first pays existing lender and disburses balance to you.

Let Me Shepherd Your LAP from Application to Disbursement

I manage each stage personally — pre-qualification, lender negotiation, legal liaison, and post-sanction follow-up. My clients typically close in 20–25 days, versus the industry average of 35–45. Book Free Consultation

About the Author: Somnath Sarkar is a loan strategy consultant with 20+ years at Axis Bank and Deutsche Bank, specialising in LAP structuring, application management, and SME funding.

Disclaimer: Timelines and processes vary by lender, property location, and applicant profile. Information is based on industry practice as of March 2026. This article is for educational purposes only and does not constitute financial or legal advice. Consult a qualified advisor for your specific situation.

Last Updated: 09 June 2026 | First Published: 09 June 2026

© 2026 Somnath Sarkar. All rights reserved.