The Short Answer

Yes — a home loan balance transfer causes a 15–30 point temporary dip in your CIBIL score. This recovers fully within 3–6 months of regular EMI payments on the new loan. Long-term impact is neutral to positive. You should not delay a financially beneficial transfer because of the small, short-lived score impact.

At Deutsche Bank, I have seen borrowers denied transfers due to CIBIL drops from multiple simultaneous inquiries — not the transfer itself, but the pattern of credit-seeking behaviour it revealed.

The CIBIL score impact of a balance transfer is one of the most common concerns I hear — and also one of the most exaggerated. A transfer will affect your score, but the effect is small, temporary, and manageable. What can cause real damage is poor sequencing: applying for 3–4 loan transfers simultaneously, taking a personal loan two months before the transfer, or failing to verify the old loan is closed correctly on your credit report after disbursement. This post walks through exactly what happens, quantifies each impact, and gives you the 5-step plan to minimise any dip.

The Short Answer: Yes, Transfer Affects Your Score — Here is How Much

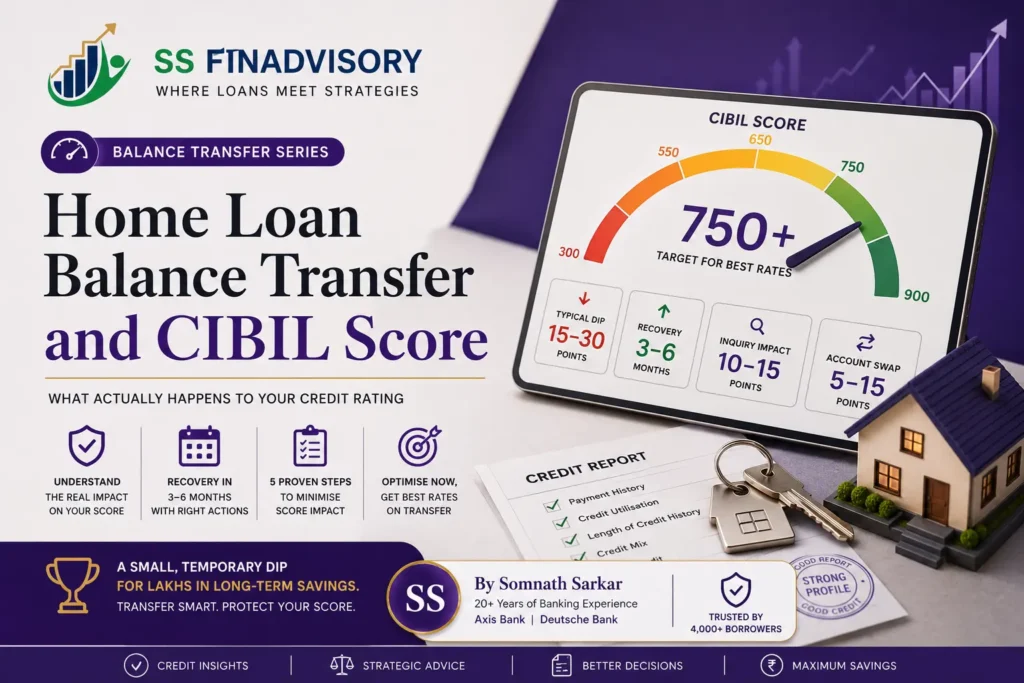

Typical Dip

15–30 pts

Combined impact from inquiry + account change

Recovery Time

3–6 mo

With regular EMI on new loan

Hard Inquiry

10–15 pts

One-time deduction at application

Account Swap

5–15 pts

Old closed + new opened

The total dip you should expect from a single, clean balance transfer is 15–30 points — assuming no other adverse factors. If your current score is 780, expect it to drop to ~755–765 for a few months, then recover. If you are at 730, expect ~700–715 temporarily, then recovery to 730+ within 6 months.

This is a small price to pay for ₹6–14 lakhs in interest savings over the loan’s life. The score concern should never override a clear financial decision — but it is worth understanding and managing.

Hard Inquiries — How Many Points Do You Lose?

Every time a lender checks your CIBIL report to evaluate a loan application, it is recorded as a “hard inquiry.” Hard inquiries impact your score because they signal active credit-seeking behaviour. A single hard inquiry typically deducts 10–15 points, and the effect fades within 6–12 months.

The multiplier effect is where borrowers get hurt. If you apply to 3 banks simultaneously to compare offers, you trigger 3 hard inquiries — a combined impact of 30–45 points. On top of that, the pattern itself looks bad: lenders see “3 home loan applications in the last 14 days” and infer you may be desperate or high-risk, potentially pricing you at a higher rate even if they approve.

The fix: use soft inquiries first. Many banks offer pre-qualification or in-principle approval processes that use soft inquiries (which do not affect your score). Get 3–4 soft-inquiry indicative offers first, pick the best 1–2, then proceed with full applications. This protects your score while still giving you leverage to negotiate.

Account Closure vs New Account: What Credit Bureaus See

A balance transfer simultaneously closes your old loan and opens a new one. The credit bureau records this as two separate events:

| Event | How It Shows on Credit Report | Score Impact |

|---|---|---|

| Old loan closed | “Closed — paid in full” | Neutral to slightly positive (shows successful closure) |

| Old loan wrongly marked “Settled” | “Settled” or “Written Off” | −50 to −100 points (major damage) |

| New loan opened | “Active” with new lender name | −5 to −10 pts initially (reduces avg account age) |

| Combined transfer effect | Net of all above | −15 to −30 pts temporary dip |

* Impact ranges indicative. Actual depends on your overall credit profile and bureau’s scoring model.

Critical verification step: 60 days after your balance transfer completes, pull your CIBIL report and confirm the old loan is marked “Closed — paid in full,” NOT “Settled” or “Written Off.” “Settled” indicates a debt the bank wrote off at a loss — it damages your score by 50–100 points and takes years to recover. If you see “Settled” on a closed balance transfer loan, raise a dispute with CIBIL immediately and demand correction from the old bank.

How Long Does the Score Dip Last?

W1

Application Week: −10 to −15 points

Hard inquiry registered. Your score drops slightly within 48–72 hours of the new bank pulling your report.

M1

Disbursement Month: Additional −5 to −15 points

New account opens, old account closes. Average account age reduces slightly, causing a secondary dip.

M3

3 Months: Partial Recovery (+5 to +10 points)

Regular EMI payments on new loan start building fresh positive history. Inquiry impact begins fading.

M6

6 Months: Near Full Recovery

Most of the dip is recovered. Your score is back within 5–10 points of pre-transfer level, and trending upward.

M12

12 Months: Net Positive

The new loan’s payment history is now firmly contributing positively. Many borrowers see scores 10–20 points higher than pre-transfer at this point.

Worried About Your CIBIL Score Before Transfer?

I will audit your current credit report, identify any red flags that could affect your transfer rate, and build a 60–90 day plan to optimise your score before application. Get a Free Credit Audit

5 Steps to Minimise CIBIL Score Impact During Transfer

- Stop all new credit applications 3–6 months before the transfer. No new credit cards, no personal loans, no auto loans, no BNPL offers. Every new inquiry adds 10–15 point dings. A clean 3–6 month window before the balance transfer inquiry is ideal.

- Pull your own CIBIL report first. Visit cibil.com and get a free report. Review for errors: wrong addresses, old closed accounts still showing “Active,” or wrongly flagged delays. Dispute and fix errors before applying — this alone can recover 20–40 points.

- Use pre-qualification (soft inquiries) before full applications. Ask banks for pre-approved or in-principle offers — these typically use soft inquiries that do not affect your score. Compare 3–4 soft-inquiry offers, pick the best 1–2, then proceed with hard inquiries only for your chosen banks.

- Pay down revolving credit 30 days before applying. Keep credit card utilisation below 30% of the limit on your statement date. High utilisation (above 50%) on the month your bank pulls your report can cost you 20–50 points — a bigger impact than the transfer itself.

- Verify closure reporting 60 days post-transfer. Check your CIBIL report to confirm the old loan shows as “Closed — paid in full.” If it shows “Settled” or is still “Active,” raise a dispute immediately. This protects you from a silent 50–100 point damage that most borrowers never notice.

These five steps, done well, can limit your transfer-related score dip to 10–15 points — half the typical impact. For the broader CIBIL improvement playbook, see our dedicated CIBIL optimisation guide in the credit cluster.

When Your Score Is Too Low for a Balance Transfer

| CIBIL Score Range | Balance Transfer Outcome | Rate Premium vs Best Rate |

|---|---|---|

| 780+ | All banks compete aggressively | Negotiable discount (−0.1 to −0.25%) |

| 750–779 | Best advertised rates offered | Base rate |

| 700–749 | Accepted with rate premium | +0.10% to +0.30% |

| 650–699 | Limited options; HFCs more likely | +0.50% to +1.00% |

| Below 650 | Most major banks decline | Typically rejected |

If your score is below 700, the economics of a balance transfer often turn negative — the rate premium you will pay offsets the benefit of transferring. Here is the recovery plan:

Phase 1 (Months 1–3): Pay down credit card balances to below 30% utilisation. Close any unused credit cards with high limits that could push utilisation up. Set up auto-pay to eliminate any late payments.

Phase 2 (Months 3–6): Do not apply for any new credit. Let existing hard inquiries age off your report. Continue all EMI and card payments on time. This alone typically adds 30–50 points over 6 months.

Phase 3 (Months 6–9): Pull your CIBIL report and dispute any errors. Old closed accounts wrongly showing “Active” or old delays that are outside the 7-year reporting window can often be corrected, adding 20–40 points.

By month 9–12, most borrowers who start in the 650–700 range can move to 720–750, unlocking better transfer rates. The extra 6–9 months of waiting often saves ₹3–8 lakhs over the loan’s life compared to transferring at a rate-penalised score.

Frequently Asked Questions

Does a home loan balance transfer reduce your CIBIL score?

Yes — temporarily, by 15–30 points. The dip comes from the new lender’s hard inquiry (10–15 pts) plus the account swap (old closed + new opened: 5–15 pts). Recovery to pre-transfer levels takes 3–6 months of regular EMI on the new loan. Long-term impact is neutral to positive.

How many credit inquiries are too many before a balance transfer?

More than 3 hard inquiries in the last 6 months is a red flag. Each inquiry deducts 10–15 points temporarily, and the pattern signals credit-hungry behaviour to lenders — potentially triggering rate penalties or rejection. Avoid all new credit applications for 3–6 months before the transfer.

How long before applying should I stop taking new credits?

Stop 3 months before at minimum, ideally 6 months. This lets recent inquiry impact fade and presents a clean credit profile. If you took a personal loan or opened new cards within 6 months, consider waiting longer — the better rate you will get more than compensates.

What CIBIL score is required for a home loan balance transfer?

750+ for best advertised rates. 700–749 gets offers at a small premium (0.1–0.3%). 650–699 faces 0.5–1% premium or rejection. Below 650, most banks decline — focus on score improvement for 6–9 months before reapplying.

Will the new home loan show differently on my credit report?

Yes — two entries: old loan as “Closed — paid in full” (the correct status), new loan as “Active” with the new lender. Payment history from the old loan is preserved as historical record. Verify “Closed — paid in full” (not “Settled”) 60 days after transfer to avoid silent 50–100 point damage.

Let Me Audit Your Credit Before You Apply

I will review your CIBIL report, flag issues, build a 60–90 day optimisation plan, and help you time the transfer for maximum rate leverage. Book Free Consultation

About the Author: Somnath Sarkar is a home loan strategy consultant with 20+ years at Axis Bank and Deutsche Bank, specialising in balance transfers, prepayment planning, and credit optimisation.

Disclaimer: CIBIL scoring methodology is proprietary to TransUnion CIBIL. Point impacts and ranges mentioned are illustrative based on industry observations and may vary based on your overall credit profile. For official scoring information, refer to cibil.com. Consult a certified credit counsellor or financial planner for advice specific to your situation.

Last Updated: 30 May 2026 | First Published: 30 May 2026

© 2026 Somnath Sarkar. All rights reserved.