Many MSMEs I have worked with got their first significant loan under CGTMSE — it is one of the most underutilised schemes in India. In February 2026, the guarantee limit doubled, and startups now qualify for ₹20 Cr coverage. If your business has strong fundamentals but limited collateral, CGTMSE deserves serious consideration before you approach traditional lenders.

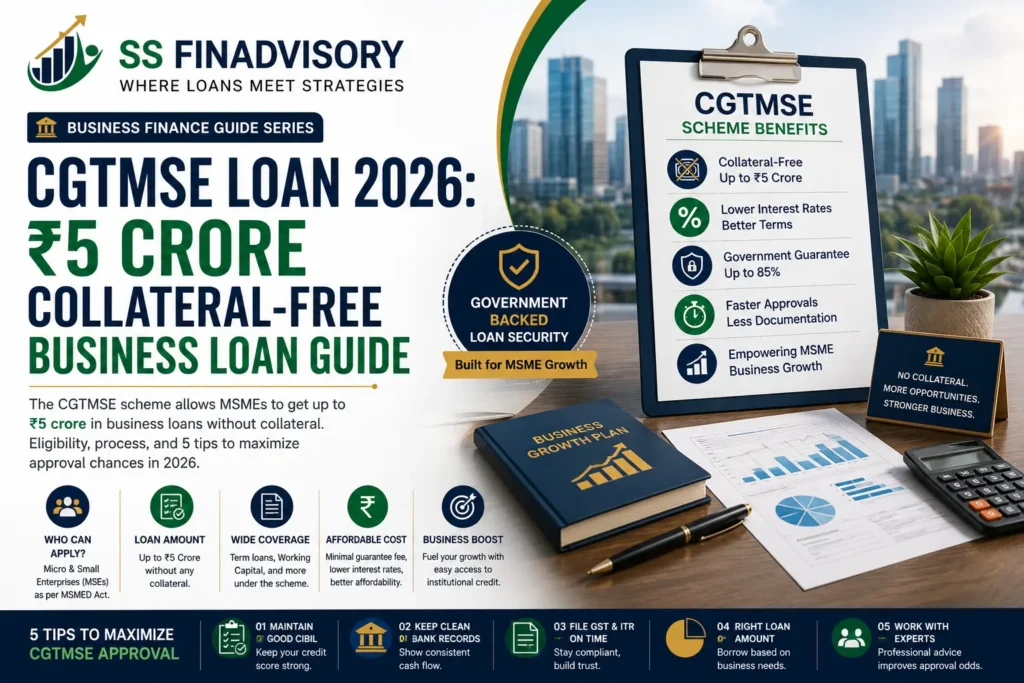

CGTMSE (Credit Guarantee Fund Trust for Micro and Small Enterprises) is the government’s answer to one of the biggest MSME financing challenges — the collateral gap. Most small businesses have strong operations but limited physical assets to pledge. CGTMSE bridges this gap by providing the lender with a guarantee cover of 75–85% of the loan amount, eliminating the bank’s need for borrower collateral. This guide walks through everything you need to know: how the scheme works, who qualifies, how much you can borrow, and the five tactics that maximise your approval odds.

What Is CGTMSE and How Does the Guarantee Cover Work?

CGTMSE is a joint initiative of the Ministry of MSME, Government of India, and SIDBI. Established in August 2000, it has grown into India’s largest credit guarantee facility for small businesses — approving guarantees worth over ₹1 lakh crore annually. The official portal is cgtmse.in, though most applications happen through participating banks rather than directly with CGTMSE.

Here is how the scheme actually works in practice:

STEP 1

You apply to a bank

Approach any CGTMSE-listed lender for a collateral-free business loan

→

STEP 2

Bank evaluates

Credit team assesses your business viability and repayment capacity

→

STEP 3

Bank seeks CGTMSE cover

On approval, bank registers loan under CGTMSE for guarantee

→

STEP 4

Loan disbursed

You receive funds; CGTMSE provides 75–85% default cover to the bank

The critical point: CGTMSE protects the lender, not you. If you default, the bank still pursues full recovery against you and your business — legal action, CIBIL damage, asset attachment all apply normally. CGTMSE only reimburses the bank for its unrecovered portion. Treat a CGTMSE loan with the same discipline as any secured loan.

Who Is Eligible for CGTMSE-Backed Loans?

Eligible Sectors

Who Qualifies

- Manufacturing industries (all types)

- Service industries — IT, consulting, healthcare, education

- Retail and wholesale trade

- Professional practices (doctors, CAs, architects)

- Agri-allied (food processing, dairy, poultry)

- Tech startups (DPIIT-recognised)

- Export-oriented MSMEs

Not Eligible

Who Does Not Qualify

- Direct agriculture / crop cultivation

- Self-help groups (SHGs)

- Loans for personal consumption

- Education/training for self-development

- Medium enterprises (investment >₹50 Cr)

- Loans already backed by collateral

- Real estate speculation

Eligibility is defined under the MSMED Act, 2006, based on two parameters: investment in plant and machinery (or equipment for service enterprises) and annual turnover. An enterprise classified as “Micro” or “Small” qualifies; Medium enterprises are excluded. The Udyam Registration Certificate is the single document that proves MSME status — obtain it at udyamregistration.gov.in before applying.

Additional lender-level requirements: clean CIBIL (personal 700+, commercial MSME Rank 1–5), 2+ years of business vintage (MUDRA-style exceptions for younger businesses), GST compliance, and a viable business plan for the proposed loan. CGTMSE does not override the bank’s underwriting — it supplements it by removing the collateral barrier.

How Much Can You Borrow Under CGTMSE in 2026?

| Borrower Category | Max Collateral-Free Loan | Guarantee Coverage |

|---|---|---|

| MSMEs (general) | Up to ₹10 Crore | 75% |

| Women entrepreneurs | Up to ₹10 Crore | 80% |

| SC/ST entrepreneurs | Up to ₹10 Crore | 85% |

| North-Eastern states / Aspirational districts | Up to ₹10 Crore | 85% |

| ZED-certified units | Up to ₹10 Crore | 90% |

| DPIIT-recognised startups | Up to ₹20 Crore | 75–85% |

| Hybrid Security (partial collateral + CGTMSE cover) | Up to ₹10 Cr uncovered portion | 75% |

* Limits effective February 2026 after RBI-CGTMSE expansion. Actual loan amount depends on your business profile, DSCR, and the bank’s internal credit policy.

Two special categories deserve attention. Hybrid Security lets you pledge partial collateral (say ₹2 Cr property) and still cover the uncovered portion of a larger loan (up to ₹10 Cr) under CGTMSE. This is useful for businesses with some assets but need more capital than the assets can secure. ZED certification (Zero Defect Zero Effect) is a quality-management certification that both improves your guarantee coverage (from 75% to 90%) and often gives you 0.25–0.50% rate concession — it pays for itself on any loan above ₹25 lakh.

Which Banks Participate in the CGTMSE Scheme?

PSU Bank · Highest volume

SBI

Dedicated MSME branches, SME Smart Score for quick evaluation. Best for traditional manufacturing.

PSU Bank

Canara Bank

Aggressive CGTMSE disbursement in recent years; strong regional presence in South India.

PSU Bank

Bank of Baroda

Strong for export-oriented MSMEs and mid-sized traders; relationship-manager-led approach.

PSU Bank

PNB & Union Bank

High CGTMSE approval volumes in northern India; good for agri-allied and food processing.

Private · Fast

HDFC Bank

15–25 day turnaround, digital documentation. Strong for services and technology MSMEs.

Private · Flexible

Axis Bank

Willing to consider borderline profiles with strong narrative. Good for first-time borrowers.

Private · Service-focused

ICICI Bank & Kotak

Specialised MSME products for doctors, CAs, architects. Higher-ticket focus (₹50L+).

Direct Lender

SIDBI

Extends CGTMSE-backed loans directly. Focuses on innovative, export-oriented, and women-led MSMEs.

Beyond these, 190+ institutions are CGTMSE Member Lending Institutions (MLIs), including all major NBFCs, regional rural banks, small finance banks, and cooperative banks. Approach 2–3 lenders aligned with your business type rather than applying broadly — shotgun applications waste CIBIL inquiries without improving odds.

Step-by-Step Application Process

- Obtain Udyam RegistrationRegister your business on the Udyam portal (free, online). This single document proves MSME status and unlocks CGTMSE, MUDRA, and all government scheme access. Takes 15 minutes.

- Pull and optimise CIBIL reportsGet both personal and commercial CIBIL reports at cibil.com. Aim for 750+ personal and MSME Rank 1–5. Dispute any errors, pay down credit card utilisation, ensure 6+ months of clean records. TIP: Start 3–6 months before applying

- Prepare your documentation packageKYC for all promoters, 3 years ITR, 2 years audited financials (for loans above ₹25L), 12 months bank statements, GST returns, Udyam certificate, and 2-page business plan with proposed use of funds.

- Identify 2–3 CGTMSE-listed lenders aligned with your businessMatch your business type to the right bank (PSU for manufacturing, private for services, SIDBI for exports/innovation). Approach them with in-principle soft inquiries first.

- Submit full application with CGTMSE requestExplicitly request CGTMSE coverage in your application. Some branches handle this automatically for MSMEs; others require you to request it specifically. Confirm before submission.

- Bank evaluates and registers with CGTMSEIf your application is approved by the bank’s credit team, they register the loan under CGTMSE through the online portal. CGTMSE issues cover within 7–10 days. Total timeline: 20–35 days for ₹10L–₹2Cr · 30–50 days for ₹2–10Cr

- Sign documents and receive disbursementAfter CGTMSE cover is registered, you sign the loan agreement and receive funds. Annual guarantee fee is typically debited upfront.

Check If Your Business Qualifies for CGTMSE

I will assess your profile, identify the best CGTMSE-listed lender for your business type, and walk you through the application — typically saving 2–3 weeks versus DIY applications that miss CGTMSE registration. Book a Free Eligibility Call

Annual Guarantee Fee — What It Costs

CGTMSE charges an Annual Guarantee Fee (AGF) of 0.37% to 2% of the sanctioned loan amount, depending on loan size, borrower category, and location. The fee is paid upfront for year one and continues annually for the loan’s tenure. Most banks pass this fee directly to the borrower as part of the loan structure.

AGF Example: ₹50 Lakh CGTMSE Loan

Loan amount₹50,00,000

Standard AGF rate1.5%

Annual guarantee fee₹75,000

Over 5-year tenure~₹3,75,000 total

Effective rate addition~0.5% over tenure

Fee is tax-deductible as business expense under Section 37(1)Net effective addition: ~0.35%

Fee concessions available: Women entrepreneurs (0.25% discount), SC/ST entrepreneurs (additional concession), businesses in North-Eastern states, aspirational districts, and LWE-affected areas (reduced slabs), and ZED-certified units (lower fees plus higher coverage). If you qualify for any of these, mention it in your application — banks do not always apply concessions automatically.

5 Tips to Maximise Your CGTMSE Approval Chances

- Get Udyam + GST + ZED in order before applying.Udyam Registration is mandatory. GST compliance for 12+ months is strongly preferred. ZED certification (even Bronze level) boosts guarantee coverage to 90% and improves negotiation position. These three together signal a serious, well-structured MSME.

- Match your business to the right CGTMSE bank.PSU banks for manufacturing and trading; private banks for services and technology; SIDBI for exports and innovation. Applying to the wrong bank for your profile wastes CIBIL inquiries. Research bank MSME focus before approaching.

- Prepare a specific, numbers-backed business plan.CGTMSE loans above ₹25L require a clear business plan. Include: current state, specific use of funds, revenue projections, repayment source, and risk mitigants. Generic plans get downsized; specific plans with cash flow projections get full amounts.

- Reconcile GST, ITR, and bank statements before submission.Discrepancies between GST turnover, ITR, and actual bank credits trigger automatic red flags. Fix inconsistencies 60–90 days before applying — file revised returns if needed, get CA-signed reconciliation for any remaining variance.

- Apply in October–December for faster processing.Banks have fresh targets in the final quarter of the financial year (Oct–Dec). Applications are processed faster and with more flexibility during this window. Avoid January–March (year-end cleanup period) and February (budget uncertainty).

Frequently Asked Questions

What is CGTMSE, and how does it help MSMEs?

Government scheme (Ministry of MSME + SIDBI) providing credit guarantee to banks/NBFCs extending collateral-free loans to MSEs. Guarantees 75–85% of loan amount against default. Enables businesses with strong fundamentals but limited assets to access institutional credit. ₹1 lakh crore+ guarantees approved annually.

Is CGTMSE available for all types of businesses?

Only for Micro and Small Enterprises engaged in manufacturing, service, or trading (per MSMED Act 2006). Eligible: manufacturing, services, retail/wholesale trade, professional practices, agri-allied. Not eligible: direct agriculture, SHGs, personal consumption loans, Medium enterprises (investment >₹50Cr).

What is the annual guarantee fee for CGTMSE?

0.37% to 2% of sanctioned loan per year. On ₹50L at standard 1.5%, AGF is ₹75,000/year. Concessions: women (0.25% discount), SC/ST, NE states, aspirational districts, ZED-certified units. Tax-deductible as business expense under Section 37(1). Effective net cost typically 0.30–0.40%.

Can existing loans be covered under CGTMSE?

No — only fresh loans. Workarounds: (1) request CGTMSE cover on loan renewal/enhancement, (2) refinance to a new lender under CGTMSE, (3) Hybrid Security model covers unsecured portion of partially-secured loans up to ₹10 Cr. Many borrowers miss these opportunities simply by not asking.

What happens if I default on a CGTMSE-backed loan?

CGTMSE protects the lender, not you. Bank initiates full recovery against you and business assets. After 12–18 months of recovery efforts, CGTMSE reimburses bank 75–85% of shortfall. Your default still damages CIBIL for 3–5 years and impairs future borrowing. Treat CGTMSE loans with same seriousness as secured loans.

Which banks have the highest CGTMSE approval rates?

Among PSU: SBI, Canara, BoB, PNB, Union Bank have highest volumes. Private: HDFC, Axis, ICICI, Kotak. SIDBI lends directly under CGTMSE. 190+ total MLIs. Approval is more about profile-bank fit than lender identity — SBI for manufacturing, HDFC/Axis for services, SIDBI for exports/innovation. Approach 2–3 aligned banks.

Let Me Structure Your CGTMSE Application

I will evaluate your MSME profile, identify the optimal bank and loan size, prepare the documentation with CGTMSE-specific framing, and liaise with the bank’s MSME team — typically closing applications in 20–25 days with full requested amounts. Book Free Consultation

About the Author: Somnath Sarkar is a loan strategy consultant with 20+ years at Axis Bank and Deutsche Bank, specialising in CGTMSE structuring, MSME funding, and government scheme utilisation.

Disclaimer: CGTMSE coverage limits, guarantee fees, and eligibility criteria are subject to change. Information verified as of March 2026 — refer to cgtmse.in and udyamregistration.gov.in for current provisions. This article is educational only and does not constitute financial advice.

Last Updated: 29 March 2026 | First Published: 29 March 2026

© 2026 Somnath Sarkar. All rights reserved.