A client improved from 680 to 735 in 8 months — it moved them from 9.5% to 8.75% on a ₹45 lakh home loan. That is ₹4.2 lakhs saved over the loan’s life. The 8-month wait and discipline required zero additional money. That return rivals what most investments offer over the same period.

Your CIBIL score does not just decide whether you get a home loan — it decides how much you pay for it over the next 15–20 years. Banks run your score through a pricing grid the moment your application arrives. A 50-point difference triggers a 0.25–0.5% rate change. On a ₹50 lakh loan over 20 years, that single number determines ₹3–5 lakhs in lifetime interest. This guide provides the exact minimums, the bank-wise comparison, and the precise rupee impact of every 50 points you gain.

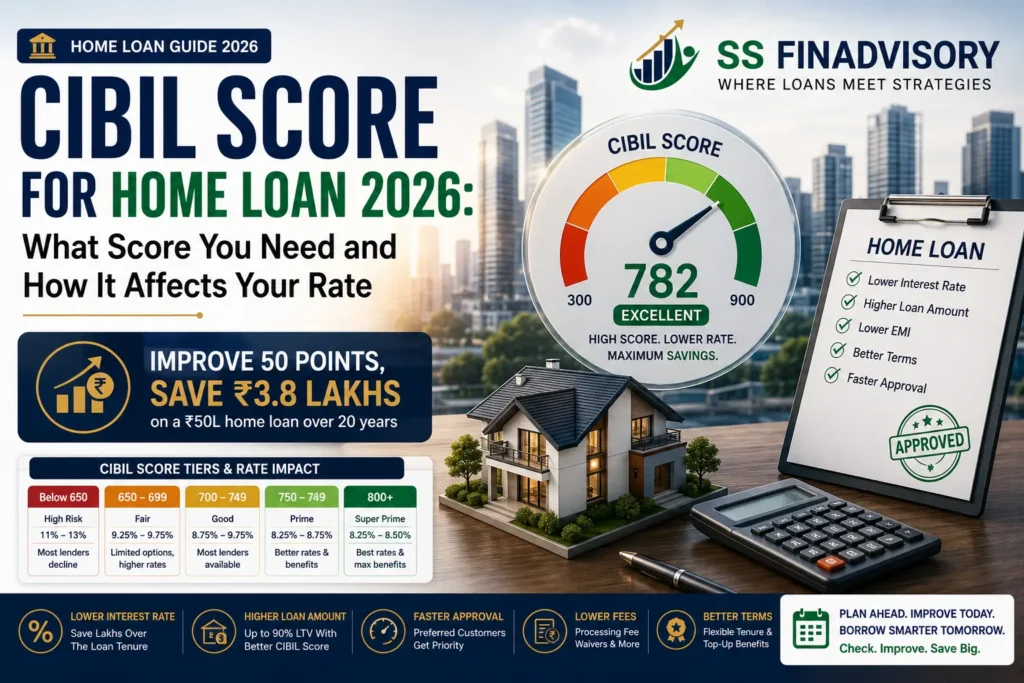

Minimum CIBIL Score for Home Loan Approval (Bank-Wise Table)

| Lender | Min CIBIL | Preferred | Rate at 750+ | Rate at 700–749 | Rate at 650–699 |

|---|---|---|---|---|---|

| SBI | 650 | 750+ | 8.50% | 8.80% | 9.40–9.75% |

| HDFC Bank | 700 | 760+ | 8.75% | 9.00% | Often declined |

| ICICI Bank | 700 | 750+ | 8.75% | 9.00% | Case-by-case |

| Axis Bank | 680 | 750+ | 8.75% | 9.10% | 9.50–9.85% |

| Kotak Mahindra | 700 | 760+ | 8.70% | 9.00% | Often declined |

| Bank of Baroda | 650 | 740+ | 8.40% | 8.75% | 9.25–9.60% |

| PNB Housing Finance | 620 | 700+ | 8.75% | 9.25% | 9.85–10.50% |

| LIC Housing Finance | 620 | 700+ | 8.65% | 9.10% | 9.75–10.25% |

| NBFCs (Bajaj / Tata) | 580 | 680+ | 9.50–10% | 10–11% | 11–13% |

* Rates indicative, March 2026, salaried profile, ₹50L loan, 20-year tenure. HFC = Housing Finance Company. Actual rates depend on lender policy and individual profile.

2026 AI underwriting insight: Banks now check your CIBIL trajectory — the direction and speed of your score over 6 months — not just today’s number. Two applicants with CIBIL 710 get different rates if one arrived from 650 (rising, positive signal) versus one arriving from 780 (falling, negative signal). Consistently improving scores get better pricing than stagnant or declining ones.

How CIBIL Score Affects Your Home Loan Interest Rate

Banks use risk-based pricing — lower credit risk means lower rate. Your CIBIL score is the primary risk input for retail home loans. Here is the rate band structure most lenders use in 2026:

| CIBIL Band | Risk Category | Typical Rate | EMI (₹50L, 20yr) | Total Interest |

|---|---|---|---|---|

| 800–900 | Super Prime | 8.25% | ₹42,603 | ₹52.24 L |

| 750–799 | Prime | 8.50% | ₹43,391 | ₹54.14 L |

| 700–749 | Near Prime | 9.00% | ₹44,986 | ₹57.97 L |

| 650–699 | Sub-prime | 9.75% | ₹47,431 | ₹63.83 L |

| Below 650 | High Risk / Declined | 10.75–12% | ₹50,803–₹54,074 | ₹71.93–₹79.78 L |

* Green = best outcomes; yellow = moderate cost; red = high cost or rejection. ₹50L loan, 20-year tenure.

The gap between Super Prime (800+) and Sub-prime (650–699) is ₹11.6 lakhs in additional interest over 20 years on this loan. Beyond rate, your score controls LTV (85–90% for 750+ vs 70–75% for 650–699, meaning a smaller down payment), processing fee waivers (₹25K–₹75K at 780+), and pre-approved offer access.

The ₹50L Loan Impact: How 50 Points Can Save ₹3.8L

Real Rupee Impact · 50-Point CIBIL Improvement

Moving from 700 → 750 on a ₹50 lakh, 20-year home loan:

At 700 CIBIL

9.00%

EMI ₹44,986/mo

At 750 CIBIL

8.50%

EMI ₹43,391/mo

Monthly saving

₹1,595

Every single month

₹3.83 Lakhs Saved

Total interest saving over 20 years from a single 50-point CIBIL improvement

Real client example: A Hyderabad IT professional improved from 680 to 735 in 8 months — primarily by reducing credit card utilisation from 68% to 22% and clearing one overdue personal loan EMI. This moved them from 9.5% to 8.75% on a ₹45 lakh home loan, saving ₹4.2 lakhs over 20 years. The improvement required zero additional financial outlay. Eight months of discipline returned ₹4.2 lakhs — that is a return that competes with any fixed-income instrument.

For larger loans, the savings scale proportionally. On ₹80 lakhs with the same 50-point improvement: ~₹6.1 lakhs saved. On ₹1.2 crore (increasingly common in metro cities): the saving exceeds ₹9 lakhs for a single 50-point CIBIL gain.

Know Your Score’s Exact Loan Impact — Free

I will model your specific loan amount against your current and target CIBIL score and show you the exact rupee savings from each 50-point improvement. 15 minutes, changes the next 20 years. Book a Free Credit-to-Loan Analysis

Which Lenders Accept Lower CIBIL Scores (650–699)?

PSU Bank

SBI & Bank of Baroda

Min CIBIL: 650

India’s most accessible home loan lenders at this score range. Rate 9.25–9.75% at 650–699. May limit LTV to 70–75%. Slower processing but most reliable approval at 650+.

PSU Bank

Canara Bank & Union Bank

Min CIBIL: 650

Strong MSME and retail home loan track record. Canara historically approves 650–680 with solid income documentation. Strong in South India.

Private (Most Flexible)

Axis Bank

Min CIBIL: 680

Most flexible major private bank. Considers 680–699 with high income and stable employment. Rate typically 9.5–9.85% at this range.

HFC

PNB Housing Finance

Min CIBIL: 620

Housing Finance Companies evaluate profiles more holistically. PNB HF accepts 620–699 at 9.75–10.5% with slower processing.

HFC

LIC Housing Finance

Min CIBIL: 620

Strong track record with lower-score borrowers. Prefers stable salaried profiles. Rates 9.75–10.25% at 650–699.

NBFC — Last Resort

Bajaj / Tata Capital

Min CIBIL: 580

Approve at 580+ with strong income but charge 11–13%. Only if urgency is extreme — improvement first saves ₹15–23L over 20 years.

NBFC maths: An NBFC at 12% vs SBI at 8.5% on ₹50L over 20 years is a difference of ₹23 lakhs in interest. Is your urgency worth ₹23 lakhs? In most cases, 6–9 months of improvement saves more than the urgency costs.

How to Improve Your Score Before Applying for a Home Loan

- Reduce credit card utilisation to below 30% (target 10–15%)Pay off balances 3–5 days before statement date — not just the due date. The reported balance is what CIBIL sees. This single action adds 20–40 points in 30–45 days. Impact: 30–45 days

- Clear all overdue accounts immediatelyAny overdue amount — credit card, EMI, or utility — actively suppresses your score every month. Pay these before any other debt action. Impact: 30–60 days

- Set up auto-debit on every obligationFuture missed EMIs are the single biggest risk during the improvement period. Auto-debit the full amount (not just minimum) to protect the score you are building. Immediate prevention

- Dispute errors at cibil.comRoughly 20% of CIBIL reports contain errors. Pull your free annual report, check every account status, raise disputes for inaccuracies. Can add 40–80 points if errors found. Impact: 30–45 days

- Freeze all new credit applications for 12 monthsEach hard enquiry costs 5–15 points. Multiple enquiries signal credit hunger and compound score damage. No new cards, personal loans, or BNPL for 12 months. Prevents -30 to -50 pts

- Keep oldest credit card activeCredit history length is 15% of your score. Never close your oldest account. Maintain it with a small monthly auto-pay purchase to keep it active without accumulating debt. Protects history length

For the complete 3-phase improvement plan covering 90 days through 12 months, see our CIBIL score improvement pillar guide. For specific strategies around credit card utilisation — the fastest single lever — see our credit utilisation guide.

The Ideal Score Timeline: Plan 6–12 Months Ahead

Now → Month 3

Fix & Stabilise

Pull CIBIL report, clear overdues, reduce utilisation below 30%, set auto-debits, dispute all errors. Target: 600→650 or 650→680.

Month 3 → Month 9

Build & Grow

6 months of zero delays, sustained low utilisation, no new credit applications. Score consolidates and grows. Target: 680→730 or 700→750.

Month 9 → Month 12

Lock In & Apply

Score stable at target for 60+ days. Select optimal lender for your score range. Apply in Oct–Dec window. Negotiate rate from strength.

The stability principle: Lenders look at score stability, not just today’s number. A score that arrived at 755 last month after being 650 six months ago looks different from a score stable at 755 for 18 months. Apply only after your target score has held for 60–90 days minimum. Stability signals structural improvement, not tactical gaming.

Frequently Asked Questions

What is the minimum CIBIL score needed for a home loan?

650 at PSU banks (SBI, BoB, Canara). 700 at private banks (HDFC, ICICI, Kotak). 620 at HFCs (PNB Housing, LIC Housing). 580 at NBFCs (last resort). Best rates (8.25–8.75%) require 750+. Aim for 700 minimum before applying, 750+ for best deal.

Can I get a home loan with a 650 CIBIL score?

Yes, limited options, higher rates. PSU banks at 9.25–9.75%. HFCs at 9.75–10.5%. Private banks often decline. Strategies: 750+ co-applicant, 30–40% down payment, FOIR below 40%, apply Oct–Dec. But 6 months to reach 700 saves ₹6–10L over 20 years — usually worth the wait.

How much lower is my interest rate with a 750+ score?

0.25–0.75% lower than 700–749. 50-point improvement (700→750) saves ₹3.83L on ₹50L/20yr. 100 points (650→750) saves ₹9.69L. Additional benefits: processing fee waiver (₹25K–₹75K), LTV up to 90%, pre-approved offers, faster processing.

Does my spouse’s CIBIL score affect joint home loan rates?

Yes significantly. Lenders evaluate both applicants and often use the lower score for rate pricing. Primary 780 + co-applicant 650 = rate priced closer to 650 tier. Ensure both are 700+ before applying jointly. If spouse is below 700, spend 6 months improving first, then add as co-applicant.

How long before applying should I improve my CIBIL score?

Start 12 months before planned application. 90 days for quick wins, 4–6 months building history, apply when stable at target for 60+ days. Minimum practical: 6 months. RBI 2026 weekly reporting means improvements show in 7–14 days — but sustained track record still matters more than recent spikes.

Find Out Your Home Loan Rate Before You Apply

I will model your current CIBIL score against 2026 home loan rates, identify the 1–3 highest-impact improvements for your profile, and match you to the right lender — all before triggering a single hard CIBIL enquiry. Book Free Consultation

About the Author: Somnath Sarkar is a home loan strategy consultant with 20+ years at Axis Bank and Deutsche Bank, specialising in credit optimisation and home loan structuring for 2,400+ families.

Disclaimer: Interest rates, CIBIL minimums, and lender policies are indicative based on industry practice as of March 2026 and subject to change. Actual rates depend on lender-specific pricing grids, income profile, property, and negotiation. This article is educational only and does not constitute financial advice.

Last Updated: 29 March 2026 | First Published: 29 March 2026

© 2026 Somnath Sarkar. All rights reserved.