At Axis Bank, I reviewed credit files for 15+ years. The patterns that separate 600 and 750+ scorers are very specific and very fixable. It is almost never about income or career — it is about six to eight behavioural habits, consistently applied for 6–12 months.

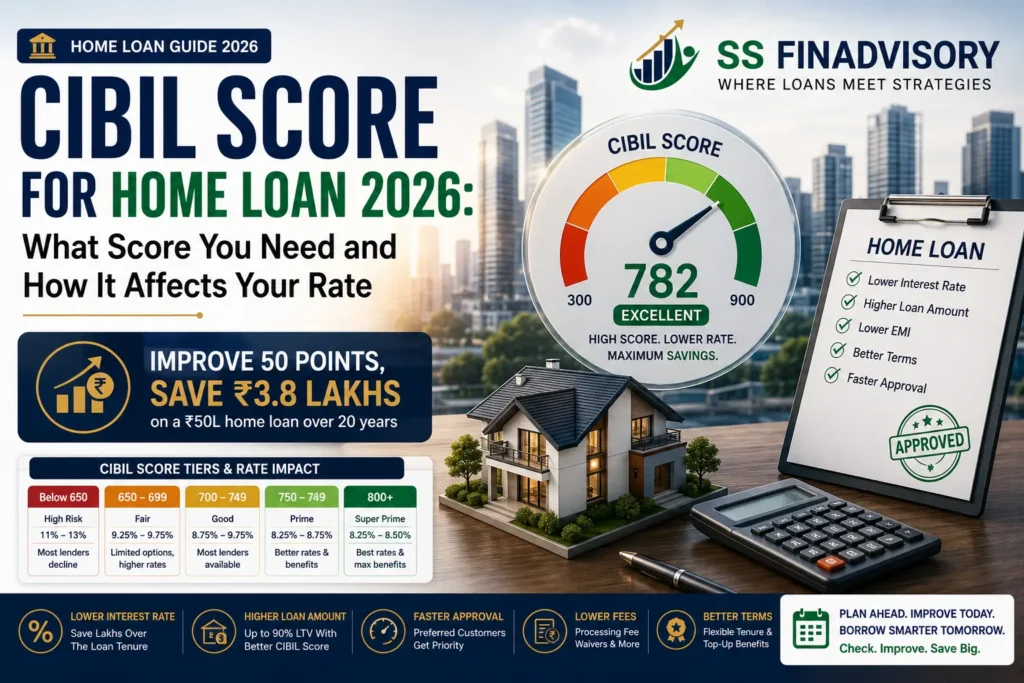

Your CIBIL score is the single most important number in your financial life. It determines whether you get a loan, what rate you pay, how much LTV you can access, and whether processing fees are waived. A 600 score and a 780 score applying for the same ₹50 lakh home loan can have a ₹10–12 lakh difference in total interest over 20 years. That is not a marginal gap — it is a down payment on a second property, a child’s higher education, or years of retirement savings.

This guide is the Cluster 4 pillar — a complete 12-month plan to move from 600 to 750+. It covers the five factors that actually move the score, three structured phases (90-day quick wins, 6-month building, 12-month excellence), the mistakes that actively damage your score, and the exact rupee impact of your score on loan economics.

Why Your CIBIL Score Matters More Than You Think (Rate Impact in ₹)

Banks do not decide loan rates arbitrarily — they run your CIBIL through a pricing grid. Here is what the score actually costs you on a typical ₹50 lakh, 20-year home loan:

| CIBIL Score | Typical Rate | Monthly EMI | Total Interest (20 yr) | Extra vs 780+ |

|---|---|---|---|---|

| 800+ | 8.25% | ₹42,603 | ₹52.24 L | Base |

| 750–799 | 8.50% | ₹43,391 | ₹54.14 L | + ₹1.9 L |

| 700–749 | 9.00% | ₹44,986 | ₹57.97 L | + ₹5.7 L |

| 650–699 | 9.75% | ₹47,431 | ₹63.83 L | + ₹11.6 L |

| Below 650 | 10.75–12% | ₹50,803–₹54,074 | ₹71.93–₹79.78 L | + ₹19.7–27.5 L |

* March 2026 indicative rates, salaried profile, ₹50L loan, 20-year tenure. Actual rates vary by lender and negotiation.

The numbers speak for themselves. Moving from 650 to 780 on this loan saves ₹9.7 lakhs. Beyond interest: processing fees are often waived above 780, LTV can extend to 85–90% (versus 70–75% below 650), and pre-approved offers kick in. Your CIBIL score is one of the highest-leverage financial numbers you will ever optimise.

Understanding the 5 Factors That Determine Your Score

CIBIL Score Factor Weightings (Industry Standard)

Payment History

35%

Credit Utilisation

30%

Credit History Length

15%

Credit Mix

10%

New Credit Enquiries

10%

* Indicative weightings. Payment history is the single most powerful factor — 65% of your score comes from payment behaviour and utilisation combined.

Payment History (35%) — timely EMI and credit card payments. A single 30-day missed payment can drop your score by 50–80 points. Negative marks stay for 7 years.

Credit Utilisation (30%) — ratio of used credit to available limit across all your credit cards. Keep below 30% on every individual card (not just overall). Paying 3–5 days before statement date ensures low reported balance.

Credit History Length (15%) — age of your oldest credit account. Never close your oldest credit card even if unused — keep it active with a small monthly expense and auto-pay.

Credit Mix (10%) — balance of secured loans (home, car, LAP) and unsecured (credit cards, personal loans). Diverse mix signals borrowing experience.

New Credit Enquiries (10%) — each hard enquiry (loan/card application) costs 5–15 points. Multiple enquiries in 30 days compound damage. Soft enquiries (self-checks at cibil.com) have zero impact.

The 90-Day Quick Wins (600 → 650)

Phase 1 · First 90 Days

Quick Wins That Deliver in 30–90 Days

Target: 600 → 650 (+50 points)

Immediate Actions (Days 1–7)

- Pull your CIBIL report at cibil.com (free once a year). Scan every line item for errors — wrong balances, accounts that are not yours, closed accounts still showing open, incorrect delay markings. Roughly 20% of CIBIL reports have errors.

- Clear any overdue amounts — overdue credit card bills, missed EMIs, or pending personal loan instalments. Even a ₹5,000 overdue is hurting your score.

- Set up auto-debit on every EMI and credit card minimum due. This eliminates accidental delays — the biggest single risk to your score.

Utilisation Reduction (Days 7–45)

- Pay credit card balances down to below 30% of each card’s limit. Target 10–15% for fastest impact. This alone can add 20–40 points in 30–45 days.

- Pay 3–5 days before statement generation date — not just the due date. The reported balance is what matters for CIBIL, not the payment itself.

- Request credit limit increases on existing cards. Higher limits automatically reduce utilisation ratio without changing spending.

Error Disputes (Days 30–90)

- File disputes for any errors found on your report. CIBIL processes disputes in 30–45 days. A legitimate dispute being resolved can add 40–80 points.

- Do not apply for any new credit. Every hard enquiry costs 5–15 points. Freeze all credit applications for the next 12 months.

Expected outcome: Most borrowers starting at 600 see 40–60 point improvement within 90 days by consistently executing these quick wins. If errors on your report are corrected, gains can be larger (80+ points possible).

The 6-Month Strategy (650 → 700)

Phase 2 · Months 3–6

Building Consistent Payment History

Target: 650 → 700 (+50 points)

Consistency Over Aggression

- 100% on-time payments for 6 consecutive months. The single most powerful long-term signal. Auto-debit all obligations so this happens automatically.

- Maintain utilisation below 30% every single month. One month of 60% utilisation can undo 2 months of good behaviour.

- Use your credit card regularly but pay in full. A dormant credit card contributes nothing to score building. Active use + full repayment is the ideal pattern.

Address Negative Legacy Items

- If you have any “Settled” accounts, negotiate with the bank to convert to “Closed” status by paying the waived-off portion. This requires formal request to the recovery team; some banks accept, some do not.

- Contact lenders for old 30-day delays and request goodwill adjustment if the delay was due to genuine circumstances (medical emergency, system error). Results vary but it costs nothing to ask.

- Do not close old credit cards — oldest card = most credit history length. Keep active with a ₹500–1,000 monthly expense on auto-pay.

Monitor and Adjust

- Check score monthly via free authorised platforms (bank apps, Paytm, CRED, Airtel Finance) — these are soft enquiries, no score impact.

- Track which actions moved the score — this pattern recognition helps in the final excellence phase.

Expected outcome: Consistent execution typically takes scores from 650 to 700+ between months 4–6. The RBI’s 2026 weekly reporting rule means improvements appear faster than before — monitor closely.

Get a Personalised CIBIL Improvement Plan

I will review your specific CIBIL report, identify the 3–5 highest-impact issues, and build a month-by-month plan to reach your target score. Most clients see 80–120 point improvement in 6 months. Book a Free 15-min Call

The 12-Month Excellence Plan (700 → 750+)

Phase 3 · Months 6–12

Reaching Excellent (750+) Territory

Target: 700 → 750+ (+50 points)

Optimise Credit Mix

- If you have only credit cards, add a small installment loan. A consumer durable EMI, small personal loan, or two-wheeler loan — serviced perfectly for 12+ months — adds credit mix and demonstrates installment discipline.

- If you have only loans, add a credit card and use it responsibly. A secured credit card against an FD works if unsecured cards are not approving.

- Avoid over-diversification — 2–4 credit cards + 1–2 loans is optimal. More than this looks like credit hunger.

Build Credit History Length

- Keep your oldest accounts open and active. Closing a 10-year-old card to open a new one can reduce average account age by years.

- Avoid applying for new credit — every new account reduces average age.

- If starting with short credit history (under 2 years), patience is the only path. Open one well-chosen credit product and let it age.

Fine-Tuning for 780+

- Target 5–10% utilisation (not just below 30%). Super-prime scorers maintain very low reported utilisation.

- Zero late payments for 12+ months. Pristine recent payment history is the final gate to 780+ territory.

- One strategic secured loan serviced perfectly. A home loan or LAP serviced for 12 months without a single delay is a powerful signal.

Expected outcome: Disciplined 12-month execution typically lands borrowers in the 750–780 range. Reaching 800+ requires 18–24 months of sustained excellence and a longer credit history.

Mistakes That Actively Damage Your Score

-50 to -80 points

Missed EMI (30+ days late)

Biggest single hit. RBI’s 2026 weekly reporting means delays show up within 7 days now, not 30-45.

-30 to -60 points

High credit card utilisation (70%+)

Even temporarily maxing a card for a genuine purchase hurts if statement captures it.

-40 to -80 points

Loan settlement or write-off

“Settled” mark stays 7 years. Negotiate to close with full payment instead.

-15 to -30 points each

Multiple hard enquiries (3+ in 30 days)

Signal of credit hunger. Space out applications — one application per 6 months maximum.

-20 to -40 points

Closing old credit cards

Reduces credit history length and total credit limit — both hurt the score.

-25 to -50 points

Guaranteeing another’s loan

If the primary borrower defaults, it hits your CIBIL exactly like your own default.

-10 to -30 points

Cheque bounces

Reflect in banking conduct; some get reported to credit bureaus via credit card auto-debit failures.

Varies widely

Ignoring report errors

20% of reports have errors. Uncorrected errors can suppress score by 40–100 points.

How to Read and Dispute Your Credit Report

CIBIL reports have six sections: Personal Information, Employment Details, Credit Summary (score + account count), Account Details (every loan/card), Enquiry Section (hard inquiries in last 2 years), and Dispute Status.

What to check carefully:

• Every account should be yours — unknown accounts signal identity theft

• Balances should match what you actually owe

• “Status” should read Active/Closed correctly (not “Settled” unless truly settled)

• Payment history rows should show “STD” (standard) for all on-time payments

• DPD (Days Past Due) column should show zero for all recent months

How to dispute errors:

- Log in at cibil.comUse your member login (created when you pulled the free report). Navigate to “Raise a Dispute” section.

- Select the specific error typeOptions: wrong balance, wrong status, account not mine, duplicate account, incorrect DPD/payment history, personal info error.

- Submit supporting documentsBank statements, NOC letters, payment proofs. Without documentation, disputes are harder to resolve.

- CIBIL forwards to the lenderThe original lender has 30 days to respond. They either confirm the error (correction happens) or contest it (dispute unresolved).

- Track dispute statusCheck weekly at cibil.com. Successful dispute resolution typically happens within 30–45 days.

- Verify score impact after correctionLarge errors being corrected (e.g., a wrong default) can boost score by 40–80 points. Pull a fresh report 45 days after resolution.

CIBIL Score and Home/Business Loan: The Rupee Impact

Beyond the ₹50L home loan example above, here is the broader picture of what your CIBIL actually controls:

Home Loan: 780+ vs 650 on a ₹75L loan over 20 years = approximately ₹15–18 lakhs total savings (interest + waived processing fee + higher LTV enabling smaller down payment).

Business Loan / LAP: 780+ vs 700 on a ₹50L business loan over 5 years = approximately ₹2.5–4 lakhs savings (rate differential of 1–1.5%). See our Business Loan Eligibility Guide for how CIBIL interacts with DSCR and other factors.

Credit Card Benefits: 780+ scorers get premium cards with 2–5% cashback, lounge access, travel benefits. 650 scorers often get basic cards with 0.5–1% rewards. Over 10 years, this differential is easily ₹1–2 lakhs in benefits.

Emergency Credit Access: High-score profiles get pre-approved offers for personal loans within 48 hours at competitive rates. Low-score profiles may face 7–15 day approval cycles at usury-level NBFC rates (22–30%) when emergency credit is needed.

The compounding effect: A 130-point CIBIL improvement (from 650 to 780) applied across a lifetime of borrowing — home loan, car loan, business loan, credit cards — conservatively saves ₹25–40 lakhs over 20 years. The time investment (12 months of discipline) has one of the highest returns on effort in personal finance.

Frequently Asked Questions

How long does it take to improve a CIBIL score?

6–12 months typically. 600→650 in 60–90 days (quick wins). 650→700 in 4–6 months (consistent payments). 700→750+ in 9–12 months (credit age + mix). RBI 2026 weekly reporting means improvements show in 7–14 days vs old 30–60 days. Consistent 12-month action can move score 100–150 points from 600 start.

What is a good CIBIL score for a home loan?

750+ ideal, unlocks best rates. Tiers: 800+ super prime (best rates, highest LTV), 750–799 prime, 700–749 (0.25–0.75% rate premium), 650–699 (conditional, 0.75–1.5% premium), below 650 (PSU/major private decline). 650 vs 780 on ₹50L home loan = ₹8–12L interest difference over 20 years.

Does checking my own CIBIL score reduce it?

No — self-checks are soft enquiries with zero score impact. Check as often as you want. Hard enquiries (lender pulls during loan/card applications) cost 5–15 points each. Free annual report at cibil.com plus free monthly checks via bank apps, Paytm, CRED, Airtel Finance. Monitor monthly to catch errors and track progress.

Can I improve my CIBIL score after loan settlement?

Yes, but takes time. Settlement stays 7 years. Recovery: (1) pay waived-off amount and ask bank to update status to “Closed”; (2) build 24+ months of positive history on top; (3) secured credit card or small loan paid perfectly for 12–18 months. Scores typically recover to 700+ within 2–3 years of disciplined rebuilding.

How many points does a missed EMI reduce your CIBIL score?

Single 30+ day missed EMI: 50–80 point drop. Depends on: starting score (higher fall more), length of delay (30d 50–60, 60d 70–90, 90d+ 100+), first vs repeat occurrence, loan type. Stays 7 years. With RBI 2026 weekly reporting, delays show in 7 days now. Set up auto-debit immediately to eliminate risk.

What is the fastest way to improve a CIBIL score?

Reduce credit card utilisation below 30% — adds 20–40 points in 30–45 days. Pay 3–5 days before statement date (not just due date). Other quick wins: clear overdues (30–50pt boost), dispute errors (40–80pt), request credit limit increases, set up auto-debit. Combined: 600→650–670 in 90 days. Beyond 700 requires 6–12 months discipline.

Let Me Review Your CIBIL Report — Free

I will analyse your specific credit report line by line, identify the 3–5 highest-impact issues hurting your score, and build a month-by-month action plan tailored to your profile. Most clients see meaningful improvement within 60–90 days. Book Free Consultation

About the Author: Somnath Sarkar is a loan strategy consultant with 20+ years at Axis Bank and Deutsche Bank, specialising in credit repair, CIBIL optimisation, and loan structuring. Has reviewed 1,000+ credit files from the lender side.

Disclaimer: CIBIL score calculations, factor weightings, and rate impacts are indicative based on industry practice as of March 2026. Actual score movements depend on individual credit profile and lender-specific pricing. Information is based on public industry standards and does not represent official CIBIL methodology. Pull your own report at cibil.com for accurate personal data. This article is educational only and does not constitute financial advice.

Last Updated: 29 March 2026 | First Published: 29 March 2026

© 2026 Somnath Sarkar. All rights reserved.